This article comes from Baker McKenzie and is authored by Paul H. Curnow, David Davies, Naoaki Eguchi, Marc Fèvre, Zoë Hilson and José Roberto Martins

In 2015 Baker McKenzie released one of the first thought leadership reports about corporate PPAs: The rise of corporate PPAs, a new driver for renewables. Since the issuance of that report there has been an almost 20% increase in the number of gigawatts of clean energy provided via corporate PPAs, with 5.4 GW of clean energy purchased by corporations in 2017 compared to the previous record of 4.4 GW in 2015, according to Bloomberg New Energy Finance’s (“BNEF”) Corporate Energy Market Outlook.

Here are where most corporations are purchasing PPAs.

Baker McKenzie has advised on many corporate PPAs throughout the world. According to the Climate Group’s RE100 Progress and Insights Report released in January 2018, direct procurement from offsite grid-connected generators has grown fourfold from 3% to 13% of RE100 members’ (corporations pledging to source 100% of their electricity from renewables at some date in the future) total renewable power consumption between 2015 and 2016.

Most of the corporate PPAs in 2017 were for wind power. (Emphasis added.) Most renewable corporate PPAs occur in the U.S. which had 2.8 GW in corporate PPA volumes in 2017, which exceeded the 2016 rate by 19% according to BNEF’s Corporate Energy Market Outlook.

Europe, the Middle East, and Africa was the second-largest market for renewable corporate PPAs in 2017, with corporates there buying 1.1 GW of clean power per BNEF. Corporate PPA volumes are increasing in Latin America and Asia Pacific due in part to increasing corporate demand for sustainable and economical energy solutions and because of regulatory changes.

Economic, green and reliability advantages sought, and by more entities

Corporations continue to look to PPAs for economic advantages such as long-term price predictability and the ability to hedge against future price increases from the grid, as well as for green and sustainable reasons. Corporate PPAs are increasingly being used in emerging markets to provide reliability and resilience by counteracting grid outages. Large multinationals are beginning to apply their sustainability pledges to their global supply chains and data centers, leading to an uptick in Asian and European corporate PPAs.

Universities are also becoming particularly active in this space due to their large energy consumption and socially conscious procurement teams. For example, in Australia, Monash University, the University of Sydney and the University of Technology in Sydney have each run corporate PPA tenders; in the U.S., Georgetown University entered into a power purchase agreement to develop a 32.5 MW offsite solar power system to provide almost half of the campus’ electricity. More industrials are entering the space; for example, some mining companies in Africa and Latin America now use corporate PPAs to source clean energy and reduce costs.

Terms shortening and lender confidence growing

In terms of market dynamics, developers prefer to sign 20 to 25-year PPAs on fixed tariffs but in the right markets will consider shortening the term to 10 years and floating tariffs. For example, in the Netherlands, it is increasingly accepted by financiers that the term of corporate PPAs has become shorter than the lifetime of the project loan (but this may gradually disappear if merchant risk increases due to decreasing subsidies). Numerous corporate PPAs have involved projects which were project financed, giving developers confidence that a corporate PPA is bankable.

New deal structures gaining popularity

Buyer consortia:

Aggregate buyer groups and consortia by which companies within the same industry or government entities within the same jurisdiction aggregate their power demand and jointly negotiate PPAs are gaining favor as a deal structure. For example, in November 2017, the Melbourne Renewable Energy Buying Group of 14 organizations, including government entities, cultural institutions, universities and corporations, became the first buying group in Australia to contract “firm supply” of electricity and green rights (large scale generations certificates (LGCs)) from a renewable energy project via a 10 year PPA.

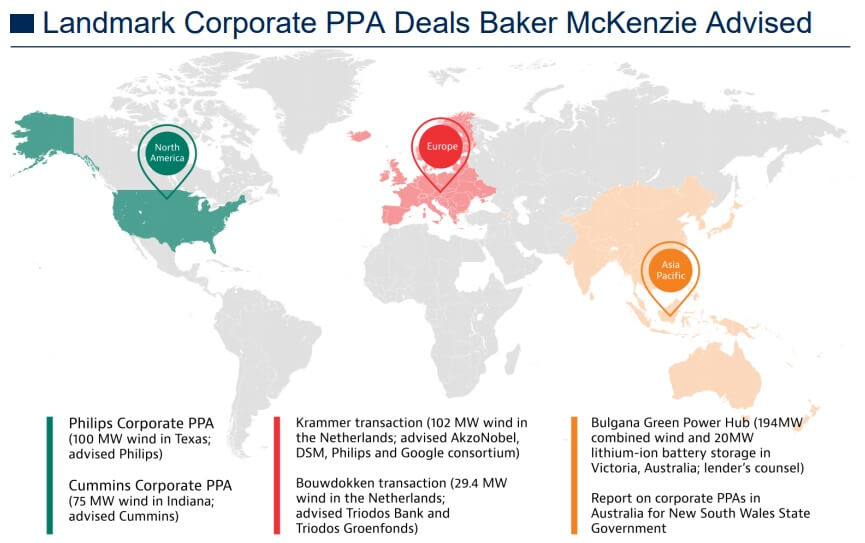

In Europe, Royal Philips, AkzoNobel, DSM and Google formed a partnership to jointly buy renewable electricity to power part of their operations in the Netherlands by entering into agreements to source electricity from the Krammer and Bouwdokken Wind Parks.

Issues to watch for in these arrangements include governance structures and risk sharing. Additionally, where consortia are purchasing power capacity together, consortium members have an increasing desire to agree that they are able to transfer all or part of their capacity share to one or more other consortium members; given the impact on the credit risk of the project company, such arrangements are key to any bankability assessment of such arrangements.

Portfolio structuring:

Smaller-scale PPA projects are increasingly being grouped within a fund or other investment structure in order to create a portfolio attractive to lenders. For example, in Asia, developers have created portfolios of rooftop solar projects, aggregating to achieve the necessary scale of at least 30-50 MW to attract finance. In this structure, the developer covers all capital costs including design, installation, full-life operation and maintenance as a turnkey project.

Similarly, in South Africa, with recent revisions to the licensing regime for IPPs and exemption from certain license requirements in respect of projects under 1MW, many developers and lenders are looking to follow a portfolio approach where a number of smaller-scale PPA projects are potentially grouped within a fund or other investment structure.

Technology’s impact

Reducing the costs for storage, price uncertainty, and a need for efficient off-grid options (particularly in the heavy industry or mining industries) has resulted in an increase of entities considering and pursuing hybrid solutions (i.e. solutions including multiple technologies such as solar PV with battery storage together with some additional gas or diesel back-up to enhance the electricity price offering and customer load profile) to meet their demand requirements while simultaneously achieving their green energy ambitions. This could promote the development of projects that become available for entering into corporate PPAs.

On the other hand, technology will allow using the current renewables infrastructure in different ways, which could lead to fewer projects that can be structured as a corporate PPA. For example, in the Netherlands, wind turbine manufacturer Lagerwey is developing a wind turbine that converts electricity into hydrogen. This hydrogen will, in first instance, be used for powering lorries. It is currently still a pilot, but if successful, given the scarcity of renewable energy projects in the Netherlands, it could affect the number of projects that become available for entering into corporate PPAs. In the longer term however, hydrogen could in the future be stored for long periods and transported via new, upgraded or existing pipelines to be converted back to electricity at the point of delivery, which will broaden the market for power. If regulatory rules are aligned across Europe to allow for cross-border corporate PPAs, this could increase the number of corporate PPAs entered into.

Regional updates

Americas

There has been significant growth in corporate PPAs in the U.S. over the past few years, with offtake agreements signed with corporates in 2017 approximately equal to all other offtakers, including utilities. This growth is coming from industrial companies and tech companies, in addition to universities and large hospital complexes. It is being driven in part by the desire of corporates to achieve their sustainability goals to satisfy the demand of their constituents both shareholders and customers Corporate renewable PPAs could be impacted by the U.S. tax reform and tariffs on solar equipment, steel and aluminum made outside of the U.S., with the tariffs deemed more unfavorable to the renewables industry than the tax reform. Despite President Trump’s intended withdrawal from Paris Agreement, many corporates continue to take it upon themselves to reduce their carbon impact, often in the form of corporate PPAs. Latin American countries such as Argentina have undergone regulatory reform to allow large consumers to sign bilateral contracts with generators that, combined with the institution of clean energy targets for corporates, is predicted to promote corporate PPA activity in the region.

For the rest of the 6-page article: https://goo.gl/so6nca

Filed Under: Policy