This executive summary and conclusions come from a white paper by Chris MacCracken, Steve Fine, and Matt Robison at consultancy ICF International. For the full white paper, pick here: http://goo.gl/i3lCrD

Executive Summary

The Clean Power Plan is not just another air quality regulation. Rather, its effect could be as broad and deep as if the United States had adopted its first real national energy plan, albeit one with less cohesiveness than a national policy because it will be designed and implemented at the state level.

As such, it will have a profound effect across the power sector. As states put programs and requirements in place to meet EPA’s state-based standards for CO2 emissions, a waterfall will reach every corner of the power sector. This waterfall will remake market dynamics and revalue assets from fossil-fuel generators to distributed renewables, from transmission to retail efficiency programs.

As such, it will have a profound effect across the power sector. As states put programs and requirements in place to meet EPA’s state-based standards for CO2 emissions, a waterfall will reach every corner of the power sector. This waterfall will remake market dynamics and revalue assets from fossil-fuel generators to distributed renewables, from transmission to retail efficiency programs.

Of course, not all state policy decisions will benefit all participants equally: There will be winners and losers, and the effects could go deep. The key to positioning will be to understand exactly what set of policy choices are most desirable to enhance value and what steps can mitigate costs and risks. In this paper, we make use of our unique insights into the Clean Power Plan as the operator of the premier power sector modeling tool for investor-owned utilities, independent power producers (IPPs),

nongovernment organizations, and the U.S. Government; the financial adviser in numerous power plant transactions; and the firm responsible for implementing 40 percent of the nation’s energy efficiency programs. We give examples showing how some of the key decisions that states will make in the next two years could drive significant swings in compliance costs, asset values, returns on investment, and business opportunities.

The Bottom Line

- The Clean Power Plan (CPP) is not just another air regulation—it has the potential to rearrange the U.S. power map. A critical determinant of winners and losers will be the states that are charged with implementing plans.

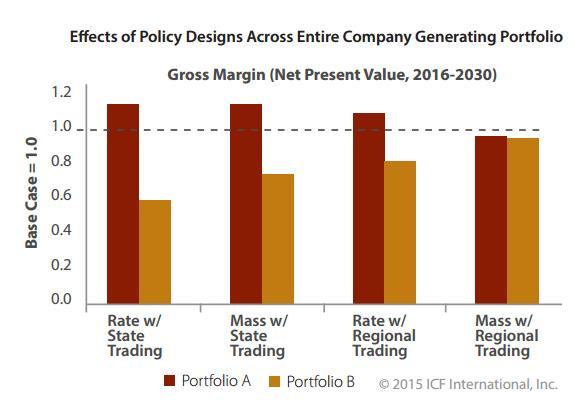

- The risks for stakeholders are real. We show how some utilities’ generation portfolios could see a 40% loss in gross margin, while individual units could see a swing of 30% in capacity factor. Utilities can substantially mitigate their costs of compliance if they can understand and achieve the policy designs that work best for their specific situation.

- We also see new business opportunities emerging not only for existing generation but also for those who can rethink their investment and business plans, and capture revenue from new energy efficiency and renewable sources. We show how one sample incremental wind unit gains 67% in gross margin under certain policies.

Drawing from market data, we demonstrate how key policy design choices across two sample states can greatly benefit one asset portfolio owner over another or bring them into parity: The “wrong” choice costs a utility a whopping 40% of its gross margin, while the “right” one loses them almost nothing. One set of policy choices increases gross margins for an incremental wind unit by 67%, siphoning value away from coal units, while others yield only moderate gains. These effects and the projection of load reductions from the growth of energy efficiency (EE) and distributed generation will seriously impact generator revenues and should cause companies to rethink everything from their planned investments to their business model. Although these threats are significant and real, the good news is some pathways are available to lower costs and take advantage of significant opportunities if stakeholders know where to look.

ICF International

www.icfinternational.com

Filed Under: News, Policy