The GWN study examined towers, jackets, permanent-magnet generators and jacket towers as manufactured by 22 companies in the U.S., Germany, and China.

The manufacturing foundation of the U.S. wind industry is in good shape but there is room to improve for the coming offshore industry. For instance, there is still potential to cut 30 to 50% on manufacturing processes used to make towers, blades, permanent-magnet generators, and jacket foundations. That is the bottom line from a presentation by Patrick Fullenkamp, Director, Technical Service with the Global Wind Network (formerly Great Lakes Wind Network, www.glwn.org). He made the remarks and more at a welding seminar sponsored by Lincoln Electric. Fullenkamp’s presentation summarized a detailed 165-page study of wind-industry manufacturing capabilities in the U.S., Germany, and China.

The study examined the four components, all sized for 3 to 5-MW turbines. To prepare for the study, Fullenkamp says he generated a value chain – a flow chart that details each step to manufacture each component. Then he visited several factories in each country and “walked the production line to understand their manufacturing steps,” he adds. The purpose was to understand the key factors determining the wind components manufacturing cost and pricing on a global base and to make recommendations that improve the competitiveness of U.S. manufacturers and eventually reduce the installed system costs.

The study examined the four components, all sized for 3 to 5-MW turbines. To prepare for the study, Fullenkamp says he generated a value chain – a flow chart that details each step to manufacture each component. Then he visited several factories in each country and “walked the production line to understand their manufacturing steps,” he adds. The purpose was to understand the key factors determining the wind components manufacturing cost and pricing on a global base and to make recommendations that improve the competitiveness of U.S. manufacturers and eventually reduce the installed system costs.

German engineers recognized the difficulty of complex pipe cuts and welds needed for a jacket tower, and so developed the red cast nodes that hold the tubes and allow simpler welds.

The study examined 22 manufacturers for the four components. “Most companies are current suppliers to land-based operations. In Europe, all manufacturers were producing in the coastal regions and most their product was for the offshore market. They have extra capacity, and with it they supplied to their land-based operations. In China, just about all manufacturing operations are located along waterways, the China Sea and Yangzi River. China, of course, supplies its own market and focuses on exports. So the initial key takeaway is that the U.S. is producing mostly in the central portion of the U.S. For offshore, the opportunities will be in the coastal regions,” says Fullenkamp. He also pointed out that now is the time to make adjustments because two offshore demo projects are slated for the Atlantic coast, and one on the Pacific coast with Principle Power. In addition, 16 other active projects are scheduled for mostly the Atlantic coast.

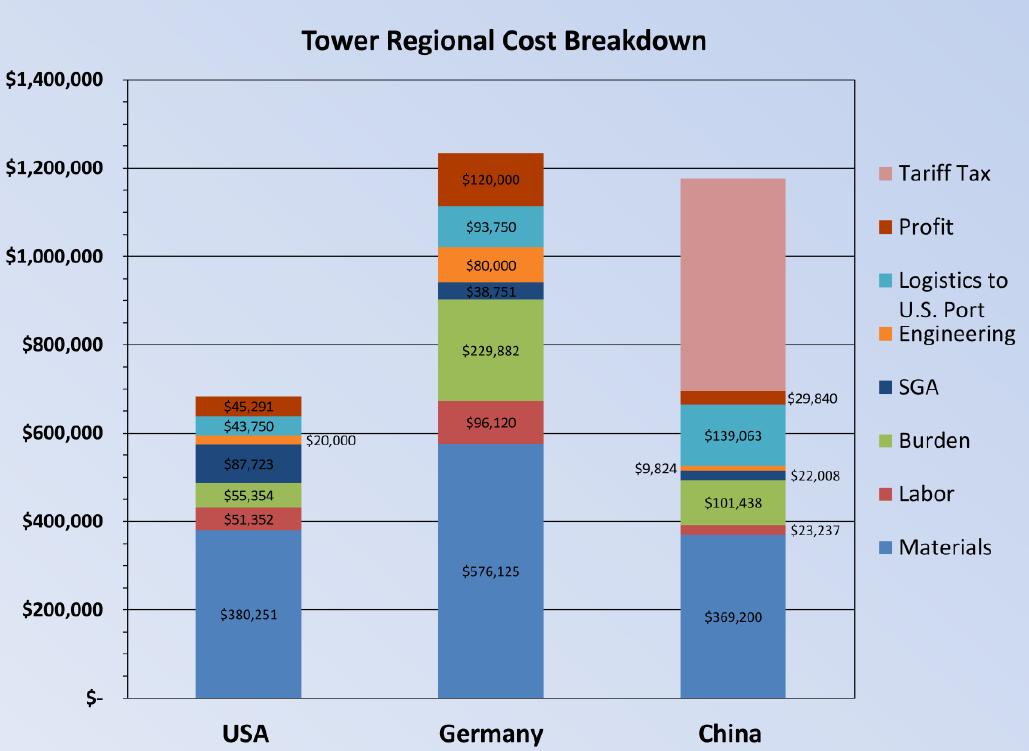

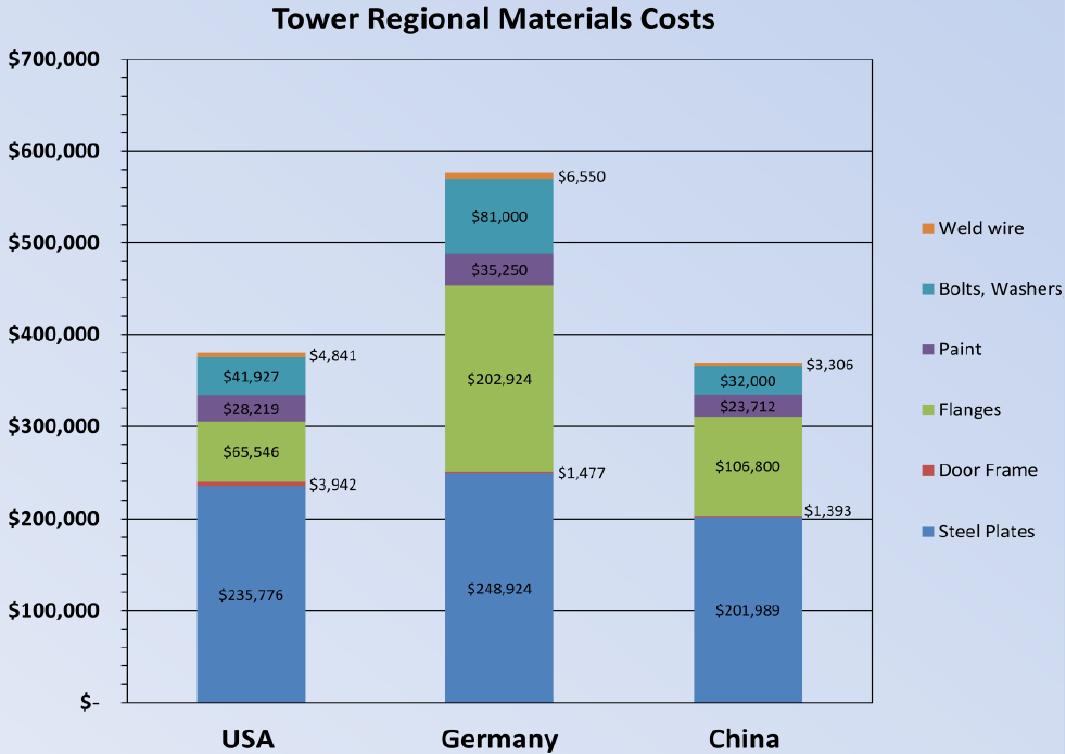

For each component, Fullenkamp identifies areas to improve. For instance, jacket foundations are 15% of capital expenditures in an offshore wind farm. For the main lattice, labor and burden or overhead is the major cost drivers at 45 to 49%. Current complex weld-interface curvatures require mostly manual welding. Material is about 29% of costs and it is mostly round pipe.

One of several report recommendations is an R&D initiative to develop a simple connection interface to cut manufacturing costs. The effort would involve tower designers, manufacturers, and welding-equipment suppliers. German engineers found that cast nodes allows simpler cuts and welds on tower tubing. Fullenkamp’s report repeats the analysis for the other components as well.

One final remark was that for 12 to 15 years, Germany has been developing a useful model for establish its offshore industry. The model seems to work. Economists there did a study in 2011 and identified their total value add. For offshore, the figure came to €$5.9 million and that will grow to close to €20 million by 2021. More importantly, German companies are willing to work with U.S. companies to repeat the success in the U.S waters.

The full report is available at www.glwn.org.

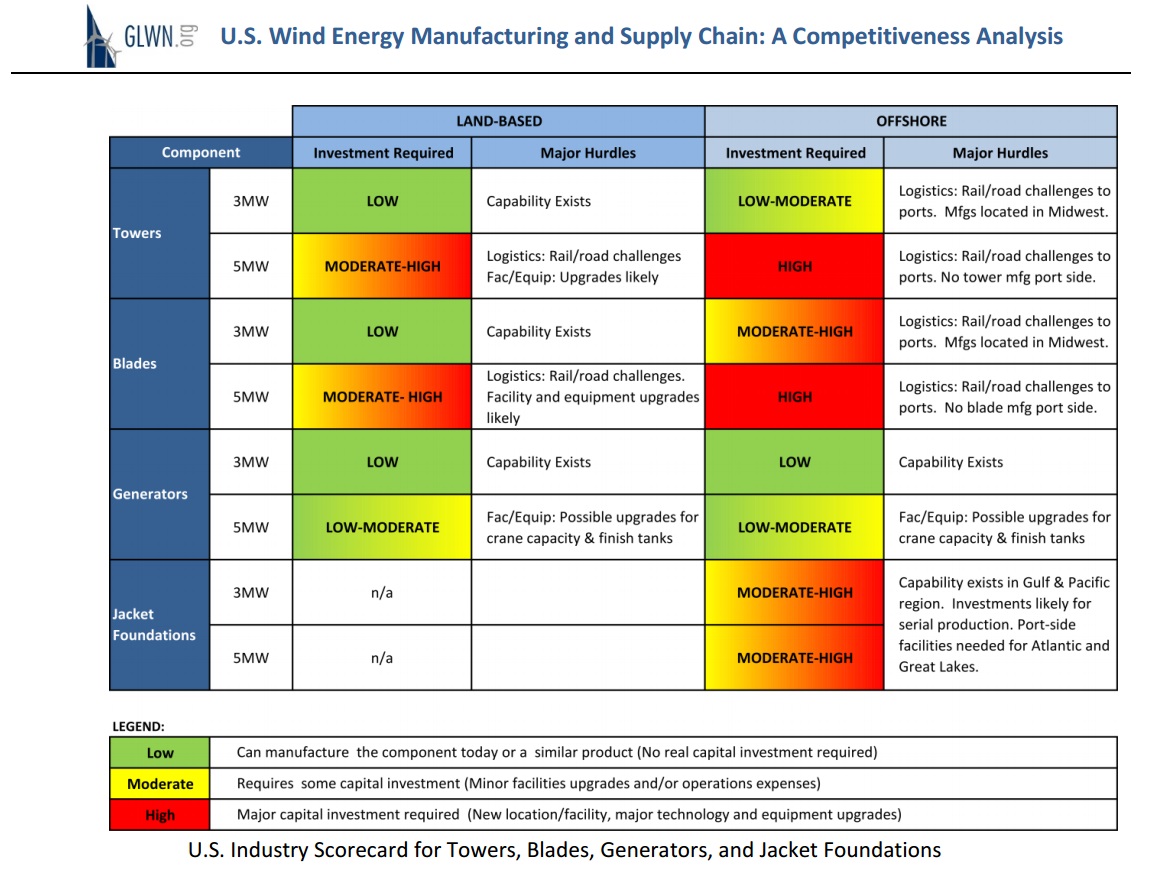

The conclusion of Fullenkamp’s report scores U.S. industries on their capabilities and highlights areas for investment.

Filed Under: Construction, News, Offshore wind, Towers