- Sales up 17% to €1,075 million

- Earnings burdened by €75 million due to structural adjustments in China and the United States

- Increase in EBIT before exceptionals to €14 million

- 50% increase in order backlog to €1,049 million

- Further sales and EBIT growth expected

Turbines like this Nordex N117 are helping the company stay profitable despite the world recession.

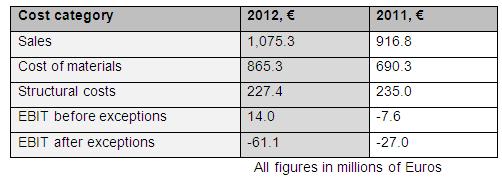

According to its provisional consolidated financial statements for 2012, sales for the Nordex Group (ISIN: DE000A0D6554) rose by 17.3% to €1,075.3 million (previous year: €916.8 million), thus matching the Management Board’s forecast. At €14 million, earnings before interest, taxes and exceptionals were also in line with the Board’s expectations (previous year: loss of €7.6 million).

The top-line growth resulted primarily from strong business in the EMEA region, where sales grew by an above-average 28% to €868.9 million (previous year: €678.6 million). The main drivers were a strong order book at the beginning of the year and growing demand in the course of the year together with an increase of more than 20% in the service business. All told, Nordex’s European business more than made up for the flat sales of its U.S. subsidiary (€191.6 million; previous year: €200.7 million) and the decline in Asian sales (€14.8 million; previous year €37.5 million).

In response to the sustained pressure on earnings caused by insufficient capacity use in America and China together with the decline in new business in these two regions, the Management Board decided to reorganise the Company’s activities in the United States and China. On the one hand, this involved the discontinued production of the rotor blade facility in Dongying, China, which resulted in a charge of €6.5 million. On the other hand, Nordex is planning adjusting capacities at the assembly plants in the light of expected order intake. The exceptional expenses arising in connection with the structural adjustments in the United States and China amounted to €75.0 million. Of this, the United States accounted for €44.8 million and China for €30 million.

The improvement in earnings before interest, taxes and exceptionals to €14.0 million (previous year: loss of €7.6 million) was mainly due to economies of scale. Moreover, Nordex was able to lower its structural costs by just under €8 million despite rising business volume. Personnel costs and, hence, the cost-cutting program adopted in 2011 yielded notable effects in this respect. The loss at the EBIT level after exceptionals amounted to €61.1 million (previous year: loss of €27.0 million). After interest and taxes, a consolidated loss of €94.4 million was sustained (previous year: loss of €49.5 million).

The improvement in earnings before interest, taxes and exceptionals to €14.0 million (previous year: loss of €7.6 million) was mainly due to economies of scale. Moreover, Nordex was able to lower its structural costs by just under €8 million despite rising business volume. Personnel costs and, hence, the cost-cutting program adopted in 2011 yielded notable effects in this respect. The loss at the EBIT level after exceptionals amounted to €61.1 million (previous year: loss of €27.0 million). After interest and taxes, a consolidated loss of €94.4 million was sustained (previous year: loss of €49.5 million).

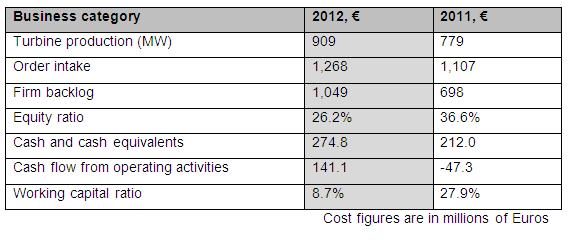

The equity ratio contracted to 26.2% (previous year: 36.6%) as a result of impairments and exceptionals. On the other hand, consolidated cash and cash equivalents rose by just under 30% to €274.8 million (previous year: €212.0 million). Cash flow from operating activities also climbed significantly to €141.1 million (previous year: net outflow of €47.3 million) due to effective working capital management. This is also reflected in the improvement in the working capital ratio to 8.7% (previous year: 27.9%).

The company’s good performance in the EMEA sales region was also reflected in new business. All in all, Nordex achieved record order intake of €1,268 million in 2012 (previous year: €1,107 million). The Europe and South Africa accounted for 94% of new orders. As a result, the Nordex Group was able to outperform the industry-wide trend and increase its backlog of firmly financed orders by over 50% to €1,049 million (previous year: €698 million). In addition, Nordex gained further conditional orders valued at roughly €1.4 billion (previous year: €1.3 billion).

The company’s good performance in the EMEA sales region was also reflected in new business. All in all, Nordex achieved record order intake of €1,268 million in 2012 (previous year: €1,107 million). The Europe and South Africa accounted for 94% of new orders. As a result, the Nordex Group was able to outperform the industry-wide trend and increase its backlog of firmly financed orders by over 50% to €1,049 million (previous year: €698 million). In addition, Nordex gained further conditional orders valued at roughly €1.4 billion (previous year: €1.3 billion).

On this basis, Nordex assumes that it will be able to achieve further growth this year. The Management Board expects sales in a range of €1.2 billion to €1.3 billion in 2013. Roughly 80% of this sales target is already covered by firm order backlog. Based on the reorganisation measures initiated in the United States and China as well as the targeted improvements in project execution and the cuts in product costs already initiated, the Management Board expects the EBIT margin to widen to 2 to 3%. Moreover, is the Board hopes to again achieve a net cash inflow from operating activities in 2013.

The key figures published in this article are preliminary. The final financial statements published about 25 March 2013, following completion of the annual audit.

Nordex

www.nordex-online.com

Filed Under: Financing, News

Curious about how good the number are when the tag on the first table says “Repower table 1 photo”.