Editor’s note: This report by consulting firm Black & Veatch provides some insight as to where the natural-gas industry is headed. It’s a compilation of opinion by those in the natural-gas industry. It’s important to the wind industry because wind and natural gas are natural allies. In a utility, the two power sources can provide the lowest cost of electricity. Although the price of gas is low, about $3.60/million BTUs late in 2013, it will rise as exports increase and utilities switch from coal. Here’s the executive summary by B&V’s Peter Abt.

The North American natural gas industry continues to hold substantial promise as an engine for sustained economic growth. However, realizing the full potential of the vast resources available will require tremendous compromise among the various stakeholders who produce, transport, distribute, trade and regulate domestic natural gas.

The North American natural gas industry continues to hold substantial promise as an engine for sustained economic growth. However, realizing the full potential of the vast resources available will require tremendous compromise among the various stakeholders who produce, transport, distribute, trade and regulate domestic natural gas.

Near-term optimism continues to increase across all respondent groups and represents a rare area of common ground. More than 95 percent of respondents stated they are “Optimistic” or “Very Optimistic” in their general outlook on future industry growth between now and 2020. This remarkable level of optimism represents a slight uptick from last year’s report, where 92% of respondents stated they were optimistic or very optimistic. Similar to the results of 2012, respondent groups also share common concerns as outlined in Table 1. Safety, by far, is the area of greatest concern and demonstrates the focus the industry directs toward achieving safe and reliable production, transmission, distribution and consumption of natural gas. (See the Appendix for an expanded Top 10 Industry Issues list.)

Technology is letting organizations automate, monitor, and collect data from cross their operations and turn it into information that supports proactive maintenance and preventative measures. However, automation also has the potential to open the door to nefarious entities through cyber attacks. The issue of cyber security has led to various regulations that are just now in the beginning stages of finalization.

Some elements of the value chain will be impacted by components of the North American Electric Reliability Corporation’s (NERC) Critical Infrastructure Protection (CIP) plan standards, while Executive Order 13636 will have far-reaching industry impacts, particularly on smaller operators. The Technology section of this report provides additional information on challenges and opportunities associated with new technologies. Regulation at the state and federal level also has tremendous influence on the industry, whether it is environmental or technology compliance or rate recovery. Significant differences exist between the Downstream and Midstream respondent groups regarding specific regulatory challenges associated with rates and cost recovery and are examined within the respective value chain sections of this report.

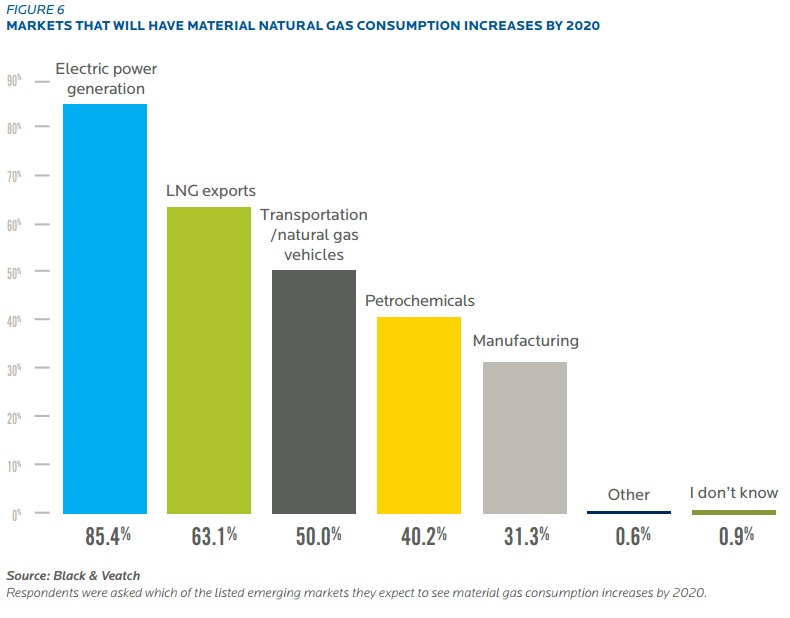

While many believe natural gas will fuel economic growth across North America, the industry is also reliant upon it, particularly the Midstream sector. More than 85% of industry respondents believe that the electric power generation industry will materially increase natural gas consumption by 2020. Today, however, much of the United States still has excess capacity as a result of significant demand reductions resulting from the 2008 recession.

The ability of pipelines to deliver gas when it is needed is of particular concern for the Downstream sector. However, electric power generators’ hesitancy to commit to firm capacity contracts makes it difficult for pipelines to attract the necessary capital needed to expand pipeline infrastructure to better serve this market. The Gas-Electric Convergence analysis in the Midstream section provides additional information and potential solutions to this challenge. generation industry will materially increase natural gas consumption by 2020. Today, however, much of the United States still has excess capacity as a result of significant demand reductions resulting from the 2008 recession.

The ability of pipelines to deliver gas when it is needed is of particular concern for the Downstream sector. However, electric power generators’ hesitancy to commit to firm capacity contracts makes it difficult for pipelines to attract the necessary capital needed to expand pipeline infrastructure to better serve this market. The Gas-Electric Convergence analysis in the Midstream section provides additional information and potential solutions to this challenge. Read the full Black & Veatch report here: http://bv.com/docs/reports-studies/2013-strategic-directions-in-the-north-american-natural-gas-industry.pdf?sfvrsn=2

Black & Veatch

Filed Under: News, Policy