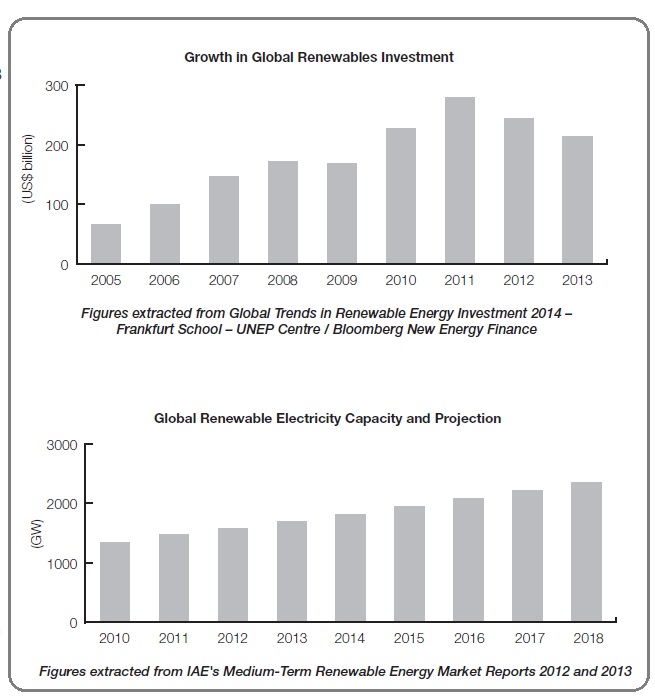

Editor’s note: This article, the introduction of a renewable-energy guide, comes from England based Clifford Chance and describes the renewable-energy incentives from about 19 countries in Europe and Asia. Introduction The last few years have seen a turbulent time for the renewable-energy sector. 2013 figures show that global investment in renewables fell significantly in both 2012 and 2013. Continuing global economic problems and uncertainty over renewable policy frameworks in key countries take a significant share of the blame. In particular, retroactive reductions in incentives in a number of European countries (in the solar sector) have caused investors to be extremely cautious about the stability of financial support mechanisms. Interestingly, part of the reason for the declining value of investment in 2012 and 2013 has been the reduction in technology costs, especially in solar and wind markets. This reduction in costs has helped deployment of renewables to continue rising despite recent falling value of investment, and deployment is projected to grow strongly at least up to 2020. In 2012, total renewable electricity generation capacity hit 1579 GW, and the International Energy Agency expects renewable electricity production to be 60% of the increase in power generation across the OECD between 2012 and 2018. Is renewable generation becoming cost effective without subsidies? In some cases, e.g. Turkey and New Zealand, onshore wind can compete effectively in the wholesale electricity markets. However, in the main, renewable generation capacity still needs financial subsidies to ensure continued growth in capacity. How does this fit with achieving targets? In Europe, there are encouraging signs of progress on meeting 2020 climate change targets. The European Commission (the Commission) expects the 20% carbon reduction and renewables targets will be achieved across the EU, although around half the Member States need to make increased efforts. However, while the Commission seeks increased carbon reductions and renewable targets in its new 2030 climate package, a number of Member States are resisting binding renewables targets as they look to other potential medium-term ways of reducing emissions. These include possibly using shale gas as an interim measure to take over from coal capacity. It remains to be seen how the potential for a shale gas bonanza in Europe will affect national policy on renewables, particularly in light of geo-political conflict in Eastern Europe, and the desirability of reducing reliance on uncertain fuel supplies. Already the UK Government has sought to push the EU to expand shale gas development to improve EU energy security. This Guide, now expanded to 19 countries across the world, gives a description of the key renewable incentive schemes in these countries, focusing principally on electricity generation. Over the years, a number of different types of subsidy mechanism have developed. Recently, Feed-in Tariff (FIT) / Feed-in Premium (FIP) schemes and, to a lesser degree, Green Certificate-type schemes have become the pre-dominant support mechanisms. For example, REN 21i notes that five FIT schemes alone were adopted in Africa and the Middle East in 2012. These are joined by a wide range of other ways of encouraging the growth of renewable energy, including tax advantages, levies and grid connection advantages (below). Incentive schemes each have advantages and disadvantages in terms of encouraging production of new capacity, ensuring flexibility faced with rising or falling costs, achieving renewables targets, providing certainty for investors, and their impacts on electricity markets. Experience of such schemes in Europe has led to one of the most significant recent developments: a new push by the European Commission to regulate the forms of financial support for renewable electricity generation on offer in Member States. Common types of renewable incentive mechanism for electricity generation Green Certificates (or Quota obligation mechanisms) Green Certificate schemes operate by awarding qualifying renewable energy generators with certificates equivalent to the amount of renewable energy generated. Some newer renewable energy technologies may receive a larger number of certificates than long-established technologies, to reflect the difference in deployment costs. Electricity suppliers are placed under an obligation to source a certain proportion of their electricity from renewables and they evidence satisfaction of their obligation by presenting Green Certificates to the regulator, which are bought from renewable generators. Penalties are payable if suppliers do not meet their obligation. Feed-in Tariffs (FIT) and Feed-in Premiums (FIP) FIT schemes are more numerous than Green Certificate schemes as they are easier to administer and generally provide renewable energy generators with greater certainty of income. FIT schemes pay a sum of money or tariff to generators on top of their electricity sales. The sum paid is often a variable amount to “top up” the sales income to an agreed level. This provides a high level of price guarantee to the generator. FIPs are a more developed form of FIT scheme, which have been adopted by a number of countries. They often involve payment of a fixed amount, irrespective of the electricity sales price received by the generator, but they can be variable payments which respond in some degree to fluctuations in market pricing. They result in generators being still exposed to electricity market prices. Other subsidies and incentive measures A wide variety of policies and support measures exist, including:

Is renewable generation becoming cost effective without subsidies? In some cases, e.g. Turkey and New Zealand, onshore wind can compete effectively in the wholesale electricity markets. However, in the main, renewable generation capacity still needs financial subsidies to ensure continued growth in capacity. How does this fit with achieving targets? In Europe, there are encouraging signs of progress on meeting 2020 climate change targets. The European Commission (the Commission) expects the 20% carbon reduction and renewables targets will be achieved across the EU, although around half the Member States need to make increased efforts. However, while the Commission seeks increased carbon reductions and renewable targets in its new 2030 climate package, a number of Member States are resisting binding renewables targets as they look to other potential medium-term ways of reducing emissions. These include possibly using shale gas as an interim measure to take over from coal capacity. It remains to be seen how the potential for a shale gas bonanza in Europe will affect national policy on renewables, particularly in light of geo-political conflict in Eastern Europe, and the desirability of reducing reliance on uncertain fuel supplies. Already the UK Government has sought to push the EU to expand shale gas development to improve EU energy security. This Guide, now expanded to 19 countries across the world, gives a description of the key renewable incentive schemes in these countries, focusing principally on electricity generation. Over the years, a number of different types of subsidy mechanism have developed. Recently, Feed-in Tariff (FIT) / Feed-in Premium (FIP) schemes and, to a lesser degree, Green Certificate-type schemes have become the pre-dominant support mechanisms. For example, REN 21i notes that five FIT schemes alone were adopted in Africa and the Middle East in 2012. These are joined by a wide range of other ways of encouraging the growth of renewable energy, including tax advantages, levies and grid connection advantages (below). Incentive schemes each have advantages and disadvantages in terms of encouraging production of new capacity, ensuring flexibility faced with rising or falling costs, achieving renewables targets, providing certainty for investors, and their impacts on electricity markets. Experience of such schemes in Europe has led to one of the most significant recent developments: a new push by the European Commission to regulate the forms of financial support for renewable electricity generation on offer in Member States. Common types of renewable incentive mechanism for electricity generation Green Certificates (or Quota obligation mechanisms) Green Certificate schemes operate by awarding qualifying renewable energy generators with certificates equivalent to the amount of renewable energy generated. Some newer renewable energy technologies may receive a larger number of certificates than long-established technologies, to reflect the difference in deployment costs. Electricity suppliers are placed under an obligation to source a certain proportion of their electricity from renewables and they evidence satisfaction of their obligation by presenting Green Certificates to the regulator, which are bought from renewable generators. Penalties are payable if suppliers do not meet their obligation. Feed-in Tariffs (FIT) and Feed-in Premiums (FIP) FIT schemes are more numerous than Green Certificate schemes as they are easier to administer and generally provide renewable energy generators with greater certainty of income. FIT schemes pay a sum of money or tariff to generators on top of their electricity sales. The sum paid is often a variable amount to “top up” the sales income to an agreed level. This provides a high level of price guarantee to the generator. FIPs are a more developed form of FIT scheme, which have been adopted by a number of countries. They often involve payment of a fixed amount, irrespective of the electricity sales price received by the generator, but they can be variable payments which respond in some degree to fluctuations in market pricing. They result in generators being still exposed to electricity market prices. Other subsidies and incentive measures A wide variety of policies and support measures exist, including:

- Carbon pricing and taxes on fossil fuels

- Tax exemptions and deductions for energy saving investments

- Priority rights to connect renewables to the grid

- Tax-efficient loan finance for renewable investment

- Guaranteed purchasers through “Supplier of last resort” mechanisms

- Exemptions from licensing requirements or discounts in fees

Download the full 52 page report here: http://www.cliffordchance.com/briefings/2014/06/renewable_incentivesapproachingmaturity-4t.html?utm_source=lexology&utm_medium=newsfeed&utm_campaign=lexology

Filed Under: Financing, News, Policy