FTI Intelligence Releases Global Wind Market Update – Demand & Supply 2015 Report

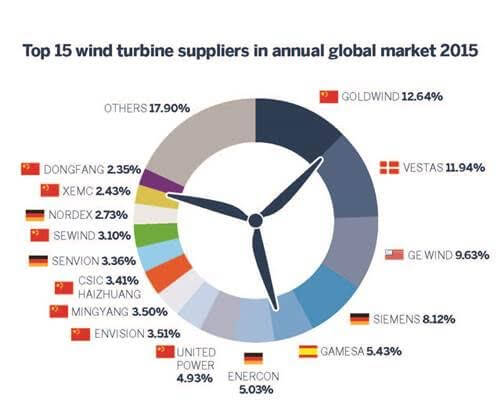

The chart ranks the world’s top 15 wind turbine OEMs.

Western wind turbine manufacturers are gearing up for more M&A (merge and acquisitions) activity as the challenge of Chinese competitors continues, according to FTI Consulting’s Global Wind Market Update – Demand & Supply 2015 report.

The global wind industry enjoyed a second consecutive record breaking year, as companies installed 63GW of new capacity, compared to 51.5GW in 2014, says FTI Intelligence. China led the way with 30.04GW, almost half the total, and Chinese companies take eight out of the top 15 places in FTI Intelligence’s ranking of the top wind turbine OEMs. Chinese manufacturer Goldwind became the world’s largest supplier of turbines, replacing historic market leader Vestas.

More than 99% of Chinese companies’ installations were in their home market in 2015, while Western companies such as Vestas, GE Enercon, Gamesa and Siemens continued to dominate in international markets. The top five companies combined accounted for almost 76% of the global market, excluding China. FTI Intelligence expects Chinese companies to increase their international market share in the next five to 10 years, however, helped by favorable government policies and an anticipated slowdown of installations in China during 2016.

Western turbine suppliers benefited strongly from the global boom in installations, with margins and share prices at buoyant levels. However, FTI Intelligence expects global installations to fall by 15% in 2016 and Western companies will face intense price competition both from their peers and Chinese competitors. M&A activity surged in 2015, with the merger of Germany’s Nordex with Spain’s Acciona Windpower, as well as the completion of GE’s acquisition of Alstom. Germany’s Siemens, currently ranked fourth, is in talks to acquire Spain’s Gamesa, in fifth place, in a move that would create a market-leading European giant.

“Chinese companies made up eight out of the leading 15 OEMs as well as the top 15 wind farm owner-operators in 2015, but their outstanding performance has been primarily driven by the market growth at home,” says Feng Zhao, Senior Director in the FTI-CL Energy practice. “With China’s market expected to grow at a steady, but less spectacular rate during the 13th Five-Year Plan period (2016-2020), we can expect to see Chinese companies increasingly challenging outside their home market, encouraged by favorable government policies.”

“Despite booming installations, competition in the global wind market is more intense than ever, and Western turbine manufacturers are getting ready for the future by stepping up M&A activity,” explains Aris Karcanias, Managing Director at FTI Consulting and Co-Lead of the Company’s Clean Energy practice. “Only those companies that can leverage global supply chain economies and tap into high-growth markets around the world will be able to compete at the very top of the market.”

Key findings in the Global Wind Market Update – Demand & Supply 2015 report include:

Detailed rankings for turbine OEMs.

Detailed wind farm owner-operators and trends of wind project ownership.

Forecasts for the wind market from 2016 through 2025 including tailor-made country profiles for established and emerging markets.

Evaluations of technology segmentation and technology trends.

The Global Wind Market Update – Demand & Supply 2015 report will be released in four parts starting with the Supply Side Analysis 2015, followed by Demand Side Analysis 2015, Technology and Project Owner-Operators. This report is part of a series of data-driven market intelligence publications evaluating competitive markets, policy, finance, technology and business models across the energy spectrum. The report is authored by members of the FTI-CL Energy practice, a cross-practice team of energy experts from both FTI Consulting and its subsidiary, Compass Lexecon.

For more on the FTI Intelligence report: www.fti-intelligence.com or at fti-intelligence@fticonsulting.com.

Filed Under: News