By Tim Buckley

Director of Energy Finance Studies, Australasia

Institute for Energy Economics and Financial Analysis (IEEFA)

Coal production is slowly losing its appeal, according to some analysts who’ve noted consumption declines in key energy markets in recent years. This trend is driven by new innovation and rapidly falling costs across the renewable and energy-efficiency sectors. New policies and investment strategies, which favor climate change and clean power production, are also affecting this trend.

The International Energy Agency (IEA) forecasts an ongoing erosion of coal’s market share in global electricity markets. In its 2015 World Energy Outlook report, the IEA shows that coal’s market share peaked at 41% in 2013 and will decline to 37% by 2020, and then drop more rapidly to 30% by 2040.

The International Energy Agency (IEA) forecasts an ongoing erosion of coal’s market share in global electricity markets. In its 2015 World Energy Outlook report, the IEA shows that coal’s market share peaked at 41% in 2013 and will decline to 37% by 2020, and then drop more rapidly to 30% by 2040.

The organization attributes this trend to the rising competition from renewable energy, and maintains that wind and solar power will rise from a relatively immaterial 6% share of global electricity generation in 2013 to 10% by 2020, and 18% by 2040.

Although interest in coal is certainly losing its edge over renewable energy sources, some analysts (including those at the Institute for Energy Economics and Financial Analysis or the IEEFA) believe the downward trend in coal shares will happen more quickly than the most recent IEA prediction. They point to IEA’s much earlier “450 Scenario” as a more realistic source, which had coal’s market share declining to 35% in 2020 and then falling rapidly to 12% by 2040. In this scenario, wind and solar power would rise in market share to 11% by 2020 and 32% by 2040.

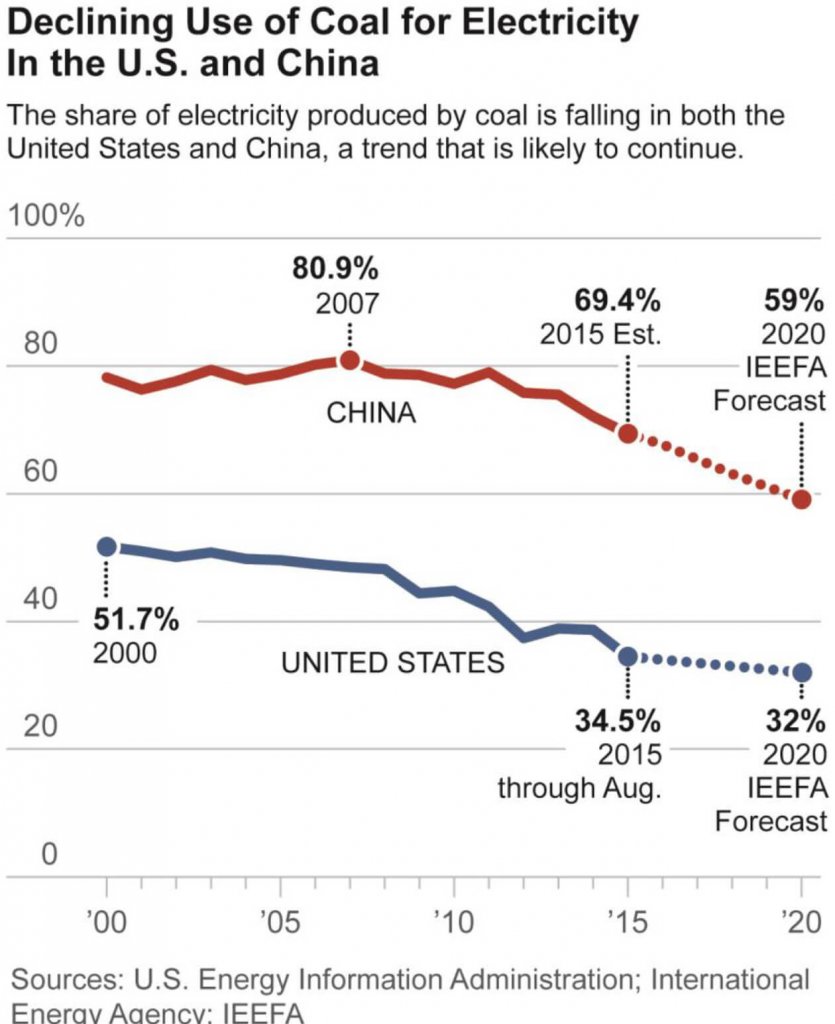

Data from the Chinese electricity market over the last two years indicates that this scenario is already becoming a reality. Although significant new coal-fired power generation has been commissioned in the country (100 GW in China over the past two years), coal-fired power utilization rates fell from 57.2% in 2013 to 53.7% in 2014. This fell even further in the first 10 months of 2015, and hit a record low of 49.3%.

In the United States, there’s a similar trend. Roughly 200 coal-fired power plants, with a combined 83 GW of capacity, have been scheduled for retirement since 2012. Record-low U.S. gas prices, record-high renewable energy construction (9 GW of wind and 8 GW of solar in 2015 alone), and a decoupling of electricity demand from economic growth are all eroding the demand for coal in the country.

Coal power’s share of U.S. electricity generation was set to decline to 35% in 2015, down from 50% a decade earlier, and global investment firm Goldman Sachs forecasts a further decline to 30% by 2025.

The lure away from coal is an environmental one, but also a cost-driven one. A key consideration in favor of renewables energy is that once built, wind and solar-powered generators are of relatively low-cost compared to coal-fired plants. Where innovation in the fossil fuel sector has typically been slow and marginally efficient, renewables are progressing differently.

Development of wind and solar technology is more akin to the type of innovation that has occurred with mobile phones, tablet devices, and the Internet. Once a critical mass has been reached in development, market shifts will occur in just a few years, rather than over several decades.

The declining state of the U.S. coal industry is the result of many factors, including innovation in renewables and decreasing wind and solar costs. But a decrease in electricity demand is also a factor, as are the regulations under the EPA’s Clean Power Plan to reduce pollution and carbon emissions in the U.S.

Investors have no choice but to acknowledge the changing energy industry. Recent published reports cite estimates that put unfunded liabilities among U.S. coal producers (including debt service, employee pension plan and healthcare obligations, and reclamation costs) at $45 billion. Such liabilities at Peabody Energy, the single largest non-governmental coal producer in the world, total $16 billion alone. This suggests that the $45 billion estimated is on the conservative side.

Make no mistake, global banks and investment firms are also noting the shift and moving funds away from higher-risk fossil fuel lending to capitalize on “green” lending opportunities.

Some examples: Bank of America set a goal of $50 billion in 2012 to provide loans and other financing for environmentally friendly energy projects over 10 years. That same year, Goldman Sachs set a 10-year target of $40 billion for investments in renewable-energy projects. In November 2015, Goldman expanded its ambition, announcing the highest lending target yet, with a commitment to invest$150 billion by 2025. (Note: This follows Goldman’s write-off and divestiture of its 2010 to 2012 $600 million of direct investments in Columbian coal mining.)

Norway’s Government Pension Fund Global, the world’s largest sovereign wealth fund, also decided to divest from the coal sector in 2015.

Coal-fired plants might never fully go away, but it’s clear change is inevitable. Future energy investments are sure to reflect the growth of renewables.

Eight signs that now is the time to invest in renewables

The Institute for Energy Economics and Financial Analysis (IEEFA) conducts research and analyses on financial and economic issues related to energy and the environment. According to their latest report, “Carpe Diem: Eight Signs that now is the Time to Invest in the Global Energy Market Transformation,” the energy market is rapidly changing. Coal is of declining interest to investors and renewable sources are on the rise.

Here are eight signs:

Here are eight signs:

- Past its prime. Coal’s share of electricity generation in key countries is declining.

- Poor demand. Demand for seaborne thermal coal is declining, and prices have collapsed. IEEFA sees internationally traded coal markets as having likely peaked in 2014 at an estimated 1,113 metric tons. The organization forecasts a further 30% decline by 2021 to 762 metric tons.

- Better prices. Innovation and economies-of-scale are working together to drive the down the capital cost of renewable energy projects. Price reductions in battery technology will compound the rate of deployment of distributed energy and energy storage technology, further undermining the commercial returns of existing fossil-fuel assets.

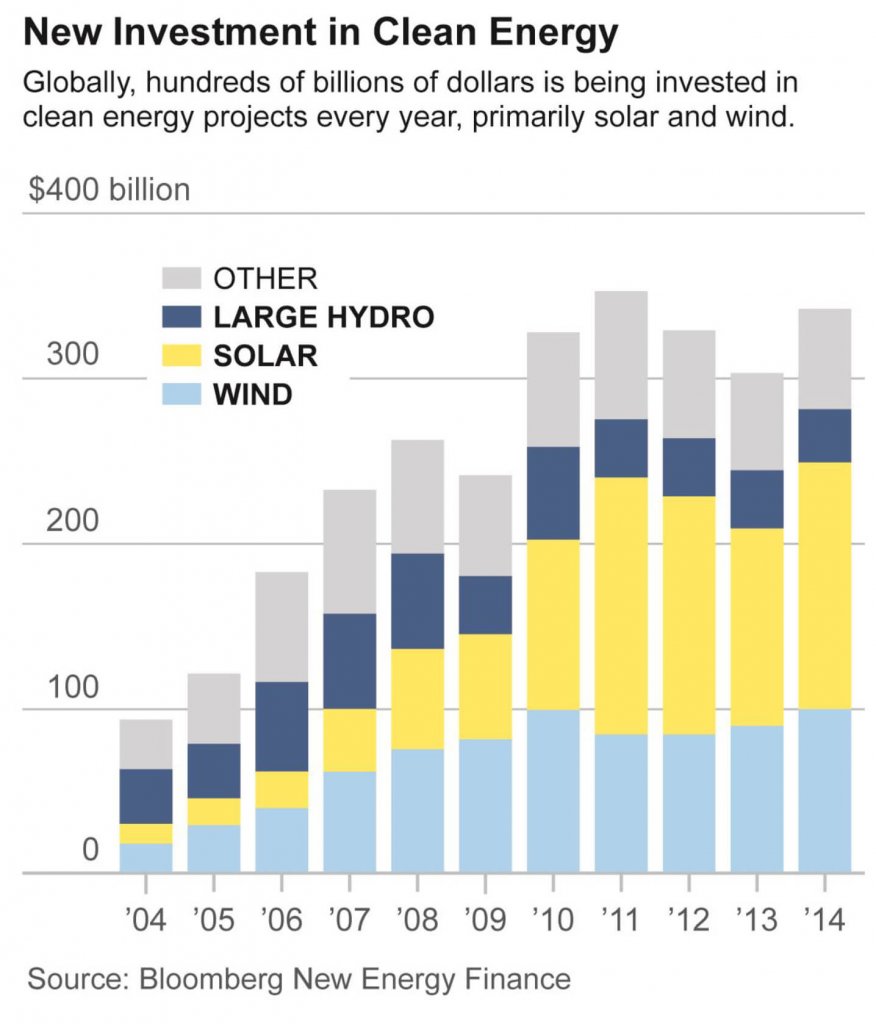

- Shifting assets. Capital is quickly moving from coal into renewables. Investors over the past decade have put $1.5 trillion into clean energy, and 2014 was a record year. These trends have triggered a shift and growing acceptance in financial markets for low-emissions investments.

- Over-committed. According to the IEEFA, coal plants have been overbuilt in many places. China has built more coal-fired plants than it can support, the U.S. is retiring many coal-fired plants, while India has fully committed to renewables.

- Financially burdened. Many coal companies are slowly finding themselves in financial distress from eroding electricity demand, energy-efficiency gains, and new climate and pollution-control regulations.

- The new black. Renewables are it. The structural decline in coal demand is becoming a common consensus amongst investors. What was once an outlier point of view — that global coal markets are in decline — is now more mainstream.

- Going green. Global banks are re-focusing. A sizeable group of financial institutions are aware of the rising regulatory and environmental pressures, and the growing risk associated with fossil-fuel assets. Banks are also aware of the rapidly falling costs across the renewable and energy-efficiency sectors. Present-day investment strategies are rooted in the recognition that an energy transformation is under way.

Filed Under: Financing