Gale E. Chan |

|

Madeline Chiampou Tully |

|

Justin Jesse |

|

Martha Groves |

|

Philip Tingle |

Senate Finance Committee Chairman Max Baucus (D-MT) recently released a proposal that would streamline energy tax incentives to make them more predictable and technology neutral.

The proposal consolidates the various tax incentives for clean electricity currently in the Internal Revenue Code (the Code) into a PTC or an investment tax credit (ITC) for all types of power generation facilities that are placed into service after December 31, 2016.

Specifically, the new proposal contemplates tax credits for electricity generated by biomass, natural gas, wind, solar, geothermal, nuclear, hydropower, and coal power generation facilities. In addition, the proposal includes new tax credits for clean transportation fuel.

The proposal comes at a time of uncertainty regarding current energy tax provisions, as some of them expired at the beginning of this year, and it is unclear whether, or when, Congress will pass an extenders bill to reinstate or extend them.

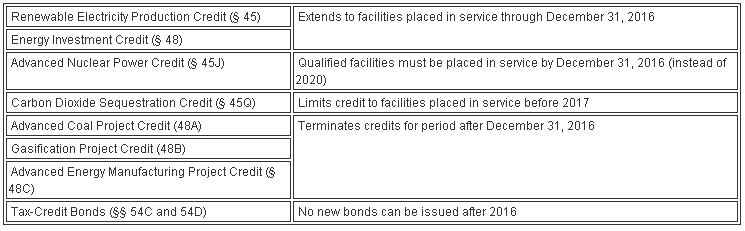

If enacted, these proposals would completely alter the current tax incentive regime for renewable energy production. The energy tax incentives impacted by the new proposal are noted in the table below.

Energy tax incentives impacted by new proposal (download for larger image).

Production Tax Credit

The proposal provides for a PTC for electricity produced at a facility in the United States and sold to an unrelated party during the year. For taxpayers that sell to related parties, the credit may still be available if the generation facility is either metered or monitored by an independent third party. The proposed PTC is equal to the number of KWh of electricity produced and sold during the year multiplied by the PTC rate, which is dependent on the facility’s greenhouse gas emissions measured in grams of equivalent carbon dioxide per kilowatt-hour (CO2e per KWh). For facilities with no greenhouse gas emissions, the PTC rate is 2.3 cents per KWh (indexed for inflation). For facilities that have greenhouse gas emissions between one and 372g CO2e per KWh, the PTC rate is reduced proportionately as a facility’s CO2e per KWh increases and approaches 372g. For example, for a facility that emits 93g of CO2e per KWh (25% of 372g), the PTC rate would be reduced by 25% to 1.7 cents per KWh. The proposed PTC is not available for generation facilities with greenhouse gas emissions greater than 372g CO2e per KWh.

For facilities that do not meet the greenhouse gas emissions standard of no more than 372g CO2e per KWh, carbon dioxide sequestration may be used to reduce the amount of measured emissions. To qualify, the sequestered carbon dioxide must be put in secure geological storage that meets certain standards to be established by the Internal Revenue Service, the Environmental Protection Agency, and the Departments of Energy and the Interior. Additionally, the carbon dioxide must be: (1) captured from an industrial source (that would otherwise release the carbon dioxide as an industrial emission of greenhouse gas), (2) measured at the source of capture and (3) verified at the point of injection. The carbon dioxide must also be captured and sequestered within the United States (or its possessions).

Investment Tax Credit

In lieu of the proposed PTC, the proposal provides for an ITC equal to a maximum of 20% of the basis of any qualified property placed into service at a generation facility after December 31, 2016. The taxpayer’s basis in the facility will be reduced by the amount of the claimed credit. Similar to the proposed PTC, the ITC credit percentage is dependent on the facility’s “cleanliness.” But because the credit is claimed in the year of investment, the percentage is based upon the facility’s anticipated greenhouse gas emissions. For facilities with no anticipated greenhouse gas emissions, the credit percentage is equal to 20%. As with the PTC, for facilities with anticipated greenhouse gas emissions between one and 372g CO2e per KWh, the ITC credit percentage is reduced proportionately as a facility’s anticipated CO2e per KWh increases and approaches 372g. Thus, for the facility that anticipates emitting 93g of CO2e per KWh (25% of 372g), the credit percentage will be 15%. If a facility’s actual emissions are significantly more than anticipated at the time it was placed into service, the ITC will be subject to recapture.

The ITC may also be available for newly installed carbon dioxide sequestration property if it is placed into service before 2017. To qualify, at least 50% of the carbon dioxide emission of the facility must be sequestered as a result of the addition of the newly installed property. This 50% rule applies regardless of whether the CO2e per KWh falls below the 372g standard.

Timing and Transition

For facilities placed into service prior to January 1, 2017, both the PTC and ITC may be available to the extent of increased power production resulting from new power production units, efficiency improvements or additions to capacity completed after December 21, 2016.

The proposal comes with an expiration date, providing that once the average greenhouse gas emission rate for U.S. generation facilities is reduced by 25% to 372g CO2e per KWh, the credits will be phased out over a three-year period. For the ITC, the maximum amount of the credit is reduced by 25% each year. For the PTC, the credit rate for the 10-year period is reduced by 25% each year.

With the introduction of these new clean energy credits, most of the tax energy incentives would be repealed or allowed to expire. Because the proposal would only apply to facilities placed into service after 2016, various current tax incentives would be extended or modified as a transition until the new credits take effect.

McDermott, Will & Emery

www.mwe.com

Filed Under: Financing, News