Pick on the image for a more readable version.

This report Overview comes from S&P Global Rating. The full report is here: https://goo.gl/AkBo5F

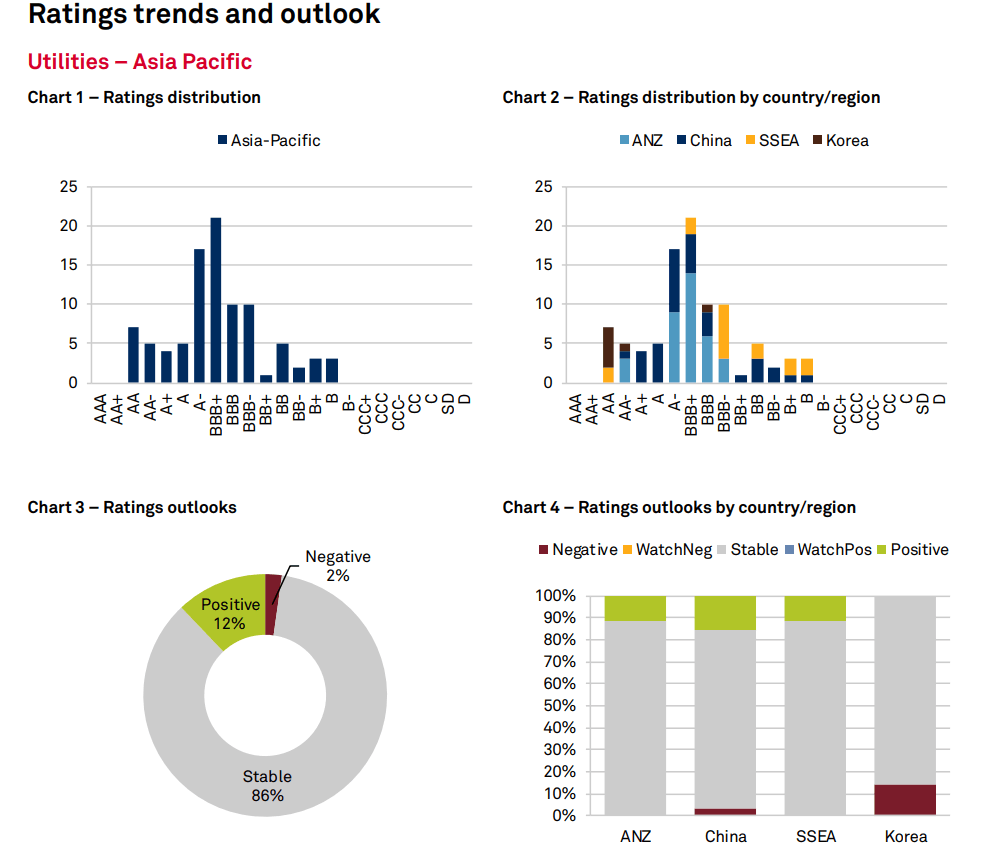

– Ratings outlook: Rating trends across utilities in Asia-Pacific remain mostly stable, supported by a stable regulatory framework and moderate demand growth. Anticipated regulatory developments and planned capital expenditure (capex) can be generally accommodated within the rating headroom. High leverage in China, India, and Indonesia provide limited headroom to accommodate regulatory surprises and negative intervention.

– Forecasts: We forecast moderate single-digit revenue growth for most regulated utilities in Asia-Pacific. China’s gas and India’s regulated utilities may see stronger growth of around 10%, driven by demand and commissioning of new projects, respectively. We forecast cash flow leverage to slightly weaken in Australia, China, and Indonesia; while Indian utilities should improve due to deleveraging.

– Assumptions: We expect economic growth to drive a moderate increase in revenues for most utilities in Asia-Pacific. We also estimate generally moderate capital spending; with a decline for China’s generation companies due to electricity sector reforms, including controls on emission and capacity additions. However, we expect elevated capex in India, Indonesia, and networks in Australia.

– Risks and opportunities: Regulatory reviews in the region will be key to greater cash flow visibility for the utilities. Indonesia and Chinese companies are exposed to higher regulatory interventions on tariff adjustments. Capital market issuances could be driven by privatization in Australia and growth capex in South and Southeast Asia amid manageable interest rate risk due to hedging or cost pass-through. However, liquidity pressures could arise in China due to high leverage and any potential stress from interest rate increases.

– Industry trends: The generation mix in Asia-Pacific is undergoing a change, with increasing penetration of renewables–though on a relatively lower base. Policy and technology developments could result in the transformation of the grid over the next two to three years, at least. China’s evolving policies on carbon trading and the merger of state-owned enterprises (SOEs) may also change the competitive landscape. China’s “Belt and Road Initiative” could significantly impact capex trends in the region, and expose some rated players to heightened risks in new markets.

Filed Under: Financing