Robert Echavaria, Head of Research, Totaro & Associates

The recent news regarding WEG acquiring the utility scale wind turbine business of Northern Power Systems (NPS) sets a new tone for the wind turbine design licensing market. WEG previously collaborated on the 2.x-MW platform through a license from NPS to WEG. It was jointly designing a 3.3-MW turbine which was already principally owned by WEG but based on the same technology architecture as the 2.x MW.

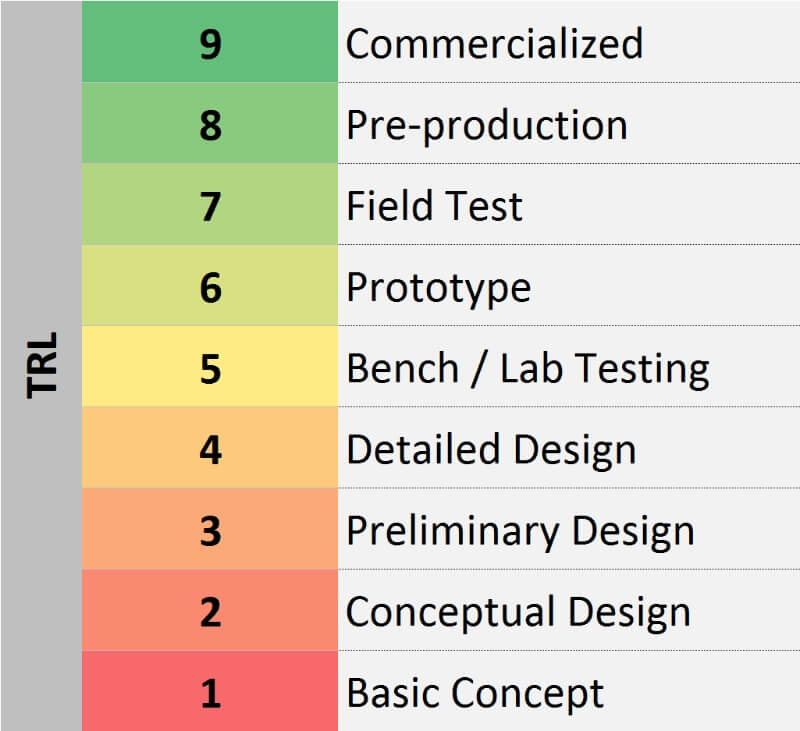

Totaro classified TRL (a state of technology devlopment) from 1 to 9.

While the specific deal value is unknown, there was likely an up-front payment for the global rights to the NPS utility scale wind business, plus the publicly acknowledged ongoing royalties for turbine sales in Brazil and the rest of the world, bringing the likely total value to approximately $30 million for NPS over the next 10 to 15 years.

This deal also gives WEG access to some extremely valuable intellectual property rights related to low voltage ride-through on a permanent-magnet direct drive (PMDD) wind turbine architecture. The entire NPS innovation portfolio is relatively mature and the portion of it which WEG now owns constitutes technology which has already been fully commercialized or is ready to enter a high rate production scheme (TRL 8 – 9).

It also provides WEG with something they have sought since the initial license was struck with NPS: the commercial rights to sell the 2.x-MW platform outside of Brazil. Since this was not provided in the 2013 license deal it hampered WEG’s ability leverage an export market from Brazil during the recent 2 year slump which they have had domestically in Brazil.

But considering this specific deal in a wider context, the evolution of the relationship for WEG and NPS is reflective of the new reality for wind turbine licensing companies in the current state of the global market. Order books from Tier 1 OEMs in major markets are fairly full for the next 3 years and Tier 2 OEMs are busy seeking global diversification in order to prop up sales numbers and maintain manufacturing production.

The heyday of design licensing where the likes of AMSC Windtec, aerodyn, Senvion (in their REpower days), W2E, Vensys, Lagerwey, and an assortment of smaller players offered turbines and engineering services cannot be sustained in a market with flat demand. Nor can it be sustained in a market with a significant global penetration of wind turbine and sub-component manufacturing capability.

In the current market environment, wind turbine bankability and finance-ability has also raised the CapEx investment requirements for OEMs. Even existing Tier 1 and Tier 2 wind turbine OEMs are dissuaded from introducing a brand new turbine design which might have a desirable step change in technology performance and LCOE due to the commercial risks related to finance and insurance.

Nevertheless, as companies evolve into the digital services sector, licensing will still be a part of the renewable energy landscape. Content licensing and digital distribution rights agreements will become more prevalent as companies come to grips with this new aspect of services and the associated business models that go with it.

Companies who can continue to innovate and create new content, new products and new services will continue to find a market for them as renewable energy continues to grow. We could see new life for technology and turbine design licensing in the coming years as demand is likely to increase.

Learn more about technology and IP licensing from the industry’s foremost experts at Totaro & Associates http://www.totaro-associates.com/licensing.

Filed Under: News, Policy